Robust portfolio optimization for factor-mimicking portfolios

A research process may produce several factor-mimicking portfolios (FMPs) that are individually credible: each has positive recent ranking evidence, an acceptable standalone backtest, and an economic rationale. That is not yet a portfolio. The sleeves may own many of the same securities, respond to the same market regime, or fail together during a factor unwind.

Allocation determines how those separate research results become one capital decision. It must decide how much confidence to place in each signal, how much diversification the sleeves actually provide, and whether a set of weights that looks efficient under average conditions remains acceptable in adverse observations. This note develops those choices from the practical question through to the mathematics, then examines them in a point-in-time comparison of five allocation rules.

Motivation

The nominal mean-variance problem is conditional on its inputs. It treats the expected-return vector and covariance matrix as known, although both are estimated from finite rolling samples. This distinction is material for FMP allocation for three reasons.

First, the expected-return score is derived from rolling ICIRRolling ICIRThe mean information coefficient divided by its standard deviation over a trailing window, usually annualized. It measures the persistence of ranking skill rather than one period’s IC.Open glossary entry →. Signal efficacy may decay, and the mean and standard deviation of ICInformation coefficient (IC)The cross-sectional correlation between a signal score and a subsequent return. Rank IC uses ranked values and measures whether the signal orders securities correctly.Open glossary entry → can change materially with the estimation window. Second, FMPs constructed from related signals may be highly correlated. A momentum sleeve and an earnings-revision sleeve may have different names while repeatedly holding the same winners. Treating them as independent allocations would overstate diversification. Third, variance is a symmetric summary of dispersion. It does not distinguish a portfolio with relatively benign adverse observations from one whose variance is driven by a small number of substantial losses.

The worst-case and CVaR extensions address the third issue directly by adding a penalty derived from the joint historical return scenarios. They do not remove estimation error or guarantee better performance. They provide a controlled way to test whether allocations remain acceptable when adverse observations enter the objective explicitly.

Problem formulation

For \(n\) candidate FMPs, let

- \(w \in \mathbb{R}^{n}\) be the vector of portfolio weights;

- \(\alpha \in \mathbb{R}^{n}\) be their expected-return scores;

- \(\Sigma \in \mathbb{R}^{n \times n}\) be their annualized covariance matrix; and

- \(R \in \mathbb{R}^{S \times n}\) contain \(S\) historical return scenarios.

The feasible set is

\[\mathcal{W} = \left\{ w \in \mathbb{R}^{n} : \mathbf{1}^{\mathsf T}w=1,\; \ell_i \leq w_i \leq u_i \right\}.\]

These constraints express portfolio policy, not merely solver mechanics. Full investment means that every dollar is assigned among the eligible FMPs and any cash or market sleeve. If the maximum weight is 35%, no single research idea can receive more than 35% of the allocation simply because its estimated return is slightly higher. Non-negative sleeve weights mean that the allocator may fund or omit an FMP, but it does not take the opposite side of the entire strategy. The FMP itself may still be a long/short, market-neutral portfolio. Cash and a market sleeve are explicit alternatives for capital rather than residuals added after optimization.

Expected-return proxy

For FMP \(i\), the expected-return proxy is derived from a time series of information coefficientsInformation coefficient (IC)The cross-sectional correlation between a signal score and a subsequent return. Rank IC uses ranked values and measures whether the signal orders securities correctly.Open glossary entry →. At date \(t\), IC measures the cross-sectional rank association between a signal score and the subsequent return:

\[\operatorname{IC}_{i,t} = \operatorname{corr}_{\mathrm{rank}} \left(f_{i,t},r_{t+1}\right).\]

Over a trailing window of \(T\) observations, the annualized information coefficient information ratio is

\[\operatorname{ICIR}_{i} = \sqrt{A}\, \frac{\overline{\operatorname{IC}}_{i}} {s\left(\operatorname{IC}_{i}\right)},\]

where \(A=252\) is the annualization convention and \(s(\cdot)\) is the sample standard deviation. The allocator maps this statistic to an expected-return score,

\[\alpha_i = c\,\operatorname{ICIR}_i,\]

with the current service using \(c=0.01\).

The quantity \(\alpha_i\) is an allocation score rather than a calibrated return forecast. Its magnitude reflects the consistency with which the signal ranked subsequent returns over the estimation window. The selected window determines the responsiveness and sampling variability of the estimate.

This choice prevents the allocator from treating a recent profitable month as evidence by itself. An FMP receives a stronger score when the underlying signal has repeatedly ranked securities correctly, not simply when the realized sleeve return happened to be high. The distinction is developed in the glossary entries for information coefficientInformation coefficient (IC)The cross-sectional correlation between a signal score and a subsequent return. Rank IC uses ranked values and measures whether the signal orders securities correctly.Open glossary entry → and rolling ICIRRolling ICIRThe mean information coefficient divided by its standard deviation over a trailing window, usually annualized. It measures the persistence of ranking skill rather than one period’s IC.Open glossary entry →.

Covariance estimator

Let \(r_t\) be the vector of FMP returns at observation \(t\). Over a covariance window of \(T\) observations, estimate

\[\widehat{\Sigma} = \frac{A}{T-1} \sum_{t=1}^{T} \left(r_t-\bar r\right) \left(r_t-\bar r\right)^{\mathsf T}.\]

The matrix contains the marginal variance of each FMP and their pairwise covariances. It is backward-looking and depends on the selected window. Short histories and highly correlated FMPs may produce a poorly conditioned estimate.

In practical terms, covariance determines whether a new sleeve adds a genuinely different source of return. Two FMPs can each have attractive ICIR and volatility in isolation but provide little diversification if their daily returns move together. Conversely, a lower-scoring sleeve may still improve the combined portfolio when its return pattern offsets risk elsewhere.

Nominal quadratic program

The nominal allocator solves

\[\underset{w \in \mathcal{W}}{\operatorname{maximize}} \quad \alpha^{\mathsf T}w - \frac{\lambda}{2} w^{\mathsf T}\widehat{\Sigma}w.\]

The first term is the portfolio expected-return score; the second is the variance penalty. The parameter \(\lambda>0\) controls their relative scale:

- smaller \(\lambda\) places more weight on the expected-return score;

- larger \(\lambda\) moves the solution toward lower variance; and

- the bounds \(\ell_i\) and \(u_i\) limit how much either estimate can concentrate the portfolio in one sleeve.

The nominal problem is a continuous convex quadratic program.

Sensitivity to estimation error

When the budget and box constraints are omitted, the first-order solution is

\[w^{*} = \frac{1}{\lambda} \widehat{\Sigma}^{-1}\alpha.\]

If \(\widehat{\Sigma}=QDQ^{\mathsf T}\), then

\[w^{*} = \frac{1}{\lambda} \sum_{j=1}^{n} \frac{q_j q_j^{\mathsf T}\alpha}{d_j}.\]

Directions associated with small eigenvalues \(d_j\) are amplified. Small changes in \(\alpha\) or in weakly identified covariance directions may therefore produce material changes in the unconstrained solution. Box constraints limit, but do not eliminate, this sensitivity.

This is the operational reason to compare optimized weights across adjacent rebalance dates. If minor input changes repeatedly move a sleeve from its lower bound to its upper bound, the portfolio is responding more to estimation noise than to a stable economic difference among the FMPs. Turnover and weight stability are therefore part of model evaluation, not only execution reporting.

Empirical scenario losses

For historical scenario \(s\), let \(r_s\) denote the vector of FMP returns. The portfolio loss is

\[L_s(w)=-r_s^{\mathsf T}w.\]

The scenario matrix is restricted to trailing observations available at the rebalance date. The resulting loss distribution is conditional on that sample and does not represent unobserved future scenarios.

The scenarios preserve joint behavior. If several FMPs lost money on the same date, that co-movement remains visible in \(L_s(w)\). Examining each sleeve's worst day separately would miss this portfolio-level concentration.

Empirical worst-case extension

The empirical worst-case loss is

\[L_{\max}(w) = \max\left(0,\max_{1\leq s\leq S}L_s(w)\right).\]

Only positive portfolio losses contribute to the penalty. The robust objective is

\[\underset{w \in \mathcal{W}}{\operatorname{maximize}} \quad \alpha^{\mathsf T}w - \frac{\lambda}{2} \left[ w^{\mathsf T}\widehat{\Sigma}w + \eta A L_{\max}(w)^2 \right].\]

Here \(\eta \in [0,1]\) is the robust-weight control. Squaring the daily loss and multiplying by \(A=252\) expresses the scenario term on an annualized variance-equivalent scale before it is combined with nominal variance.

This formulation is sensitive to one observation by construction. Its use therefore places substantial weight on data quality and window selection.

The worst-case mode is most informative when the relevant question is specific: would the proposed allocation have placed too much capital in the combination of FMPs that failed together on the most adverse observed date? It is deliberately conservative and should be accompanied by inspection of the scenario that binds the result.

Empirical CVaR extension

CVaR replaces the single largest loss with the average loss in the selected tail. Sort scenario losses from largest to smallest,

\[L_{(1)}(w) \geq L_{(2)}(w) \geq \cdots \geq L_{(S)}(w),\]

and for confidence level \(q\) define

\[m=\left\lceil(1-q)S\right\rceil, \qquad \widehat{\operatorname{CVaR}}_{q}(w) = \frac{1}{m} \sum_{j=1}^{m}L_{(j)}(w).\]

The current implementation then sets

\[T_q(w) = \max\left( 0, \widehat{\operatorname{CVaR}}_{q}(w) \right)\]

and solves

\[\underset{w \in \mathcal{W}}{\operatorname{maximize}} \quad \alpha^{\mathsf T}w - \frac{\lambda}{2} \left[ w^{\mathsf T}\widehat{\Sigma}w + \eta A T_q(w)^2 \right].\]

For \(q=0.95\), the statistic averages approximately the largest five percent of observed losses, with a minimum tail size of one observation.

CVaR is less dependent on one date than the worst-case statistic. It asks whether the proposed weights performed acceptably across a set of adverse observations. This is useful when no single historical event should determine the portfolio, but repeated losses in similar conditions remain relevant to allocation.

Numerical solution of the robust modes

The nominal problem is solved continuously. The worst-case and CVaR modes instead

enumerate feasible points on the simplex using the configured grid_step and

select the point with the highest robust score.

- a smaller grid step gives finer weight resolution but increases computation;

- a larger step is faster but may miss a better point between grid values;

min_weightandmax_weightmust leave at least one feasible simplex point; and- the robust result is the highest-scoring evaluated grid point rather than an exact continuous optimum.

The implementation bounds the number of evaluated points. Computational cost therefore increases with the number of FMPs and the requested grid resolution.

Parameterization

Estimation windows

icir_window_daysdetermines the observations used to estimate each expected-return score. Short windows respond more quickly but have greater sampling variability.cov_window_daysdetermines both the sample covariance matrix and the historical scenario set. Changing this window changes estimated correlations and the losses available to the robust penalty.

Objective controls

lambda_riskscales the complete risk term relative to the expected-return score. Larger values reduce the tolerance for estimated variance and tail loss.robust.weightcontrols the contribution of the variance-equivalent tail term. A value of zero recovers the nominal objective.cvar_alphasets the CVaR confidence level. Higher values use a smaller and more adverse subset of the scenario-loss distribution.

Constraints and numerical resolution

min_weightandmax_weightdefine the feasible box and limit concentration.grid_stepdetermines the resolution of the worst-case and CVaR search. Finer resolution increases the number of candidate portfolios evaluated.

Benchmark allocators

The available methods impose different information requirements:

Allocation methods and their information requirements

| Method | Expected-return input | Covariance input | Tail scenarios |

|---|---|---|---|

| Equal weight | No | No | No |

| ICIR-proportional | Rolling ICIR | No | No |

| Hierarchical risk parity | No explicit alpha | Yes | No |

| Nominal Markowitz | Rolling ICIR | Yes | No |

| Robust Markowitz | Rolling ICIR | Yes | Worst-case or CVaR |

Equal weighting provides a low-estimation benchmark. ICIR-proportional allocation isolates the expected-return ranking from the covariance estimate. Hierarchical risk parity uses covariance structure without an explicit expected-return score. The nominal and robust Markowitz variants incorporate the complete objective.

An empirical walk-forward comparison

To make the discussion concrete, we constructed six FMP sleeves from alternative portfolio constructions of one cross-sectional signal: full-universe equal and z-score weighting, equal-weight 10%, 20%, and 33% tails, and z-score-weighted 10% tails. The exercise is deliberately narrow. Holding the signal fixed makes the comparison about allocation rather than about which forecasting model was better.

Every method received the same point-in-time sleeve returns and IC observations. Weights used a one-day lag and were reconsidered every 21 trading days. The expected-return window was 63 observations, the covariance and scenario window was 126 observations, individual sleeve weights were constrained to \([0,0.5]\), and allocation turnover was charged 5 basis points. The robust method used 95% empirical CVaR, \(\eta=0.5\), and a 10 percentage-point simplex grid.

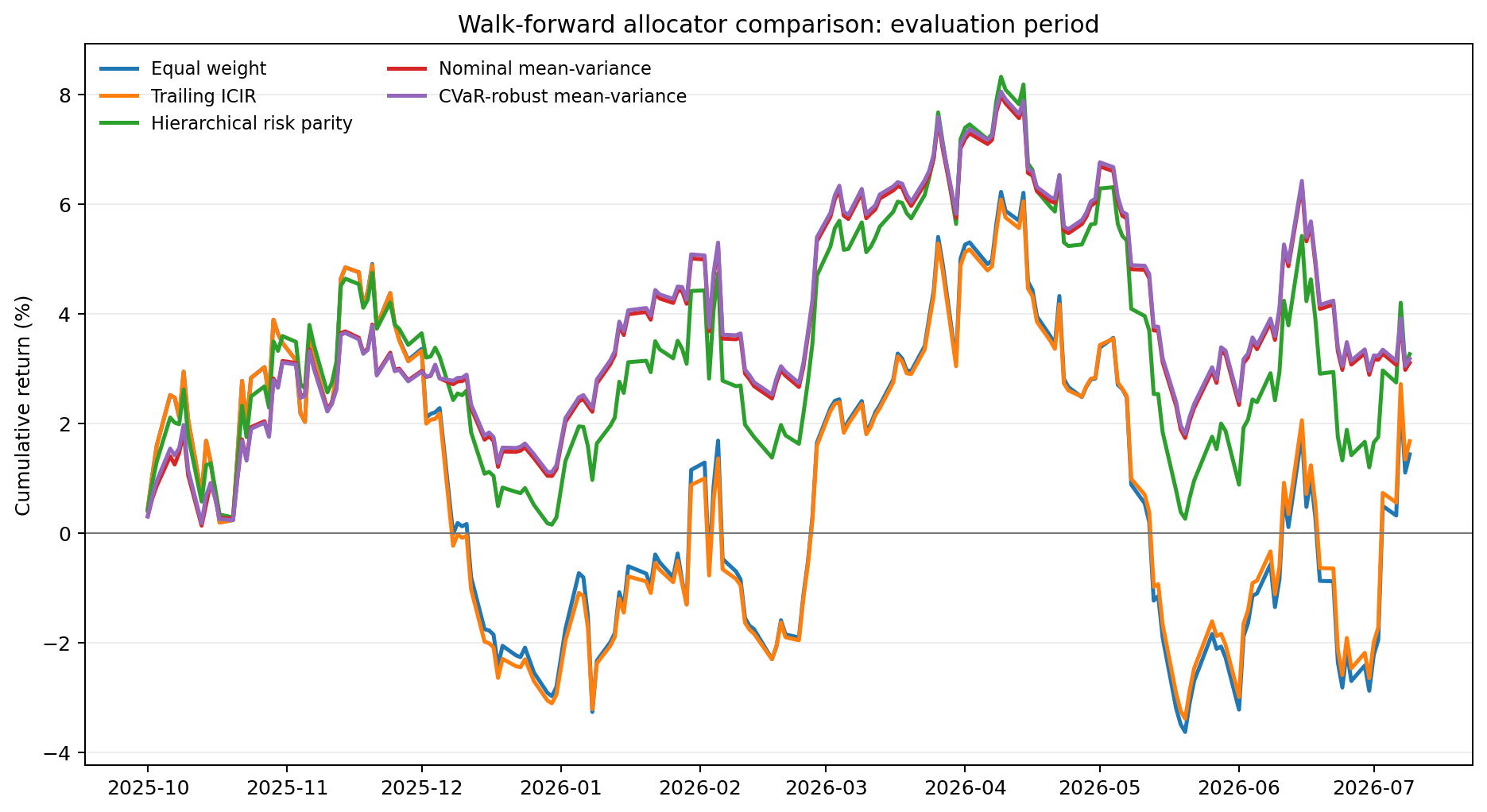

The production history ran from 9 July 2024 through 9 July 2026. Dates without usable factor values were skipped before the common matrix was formed. After the 63-observation warm-up, all five methods shared 413 available trading-day observations. The evaluation interval was fixed in advance as 1 October 2025 through 9 July 2026, containing 195 observations. No parameters were selected from that interval.

Evaluation-period performance, 1 October 2025–9 July 2026

| Method | Annualized return | Sharpe | Max drawdown |

|---|---|---|---|

| Equal weight | 1.86% | 0.21 | 9.28% |

| Trailing ICIR | 2.17% | 0.24 | 8.93% |

| Hierarchical risk parity | 4.24% | 0.48 | 7.45% |

| Nominal mean-variance | 4.04% | 0.56 | 5.78% |

| CVaR-robust mean-variance | 4.13% | 0.58 | 5.78% |

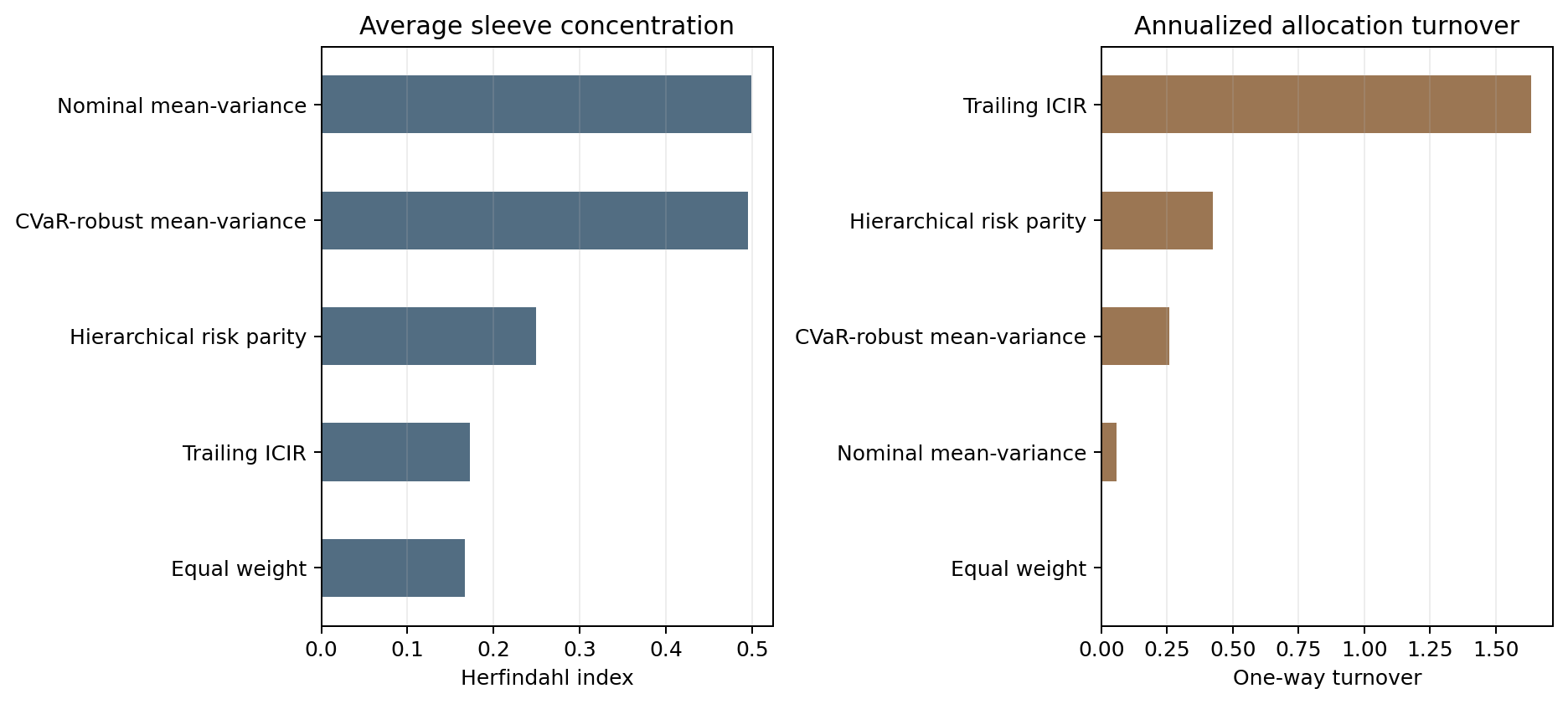

Evaluation-period allocation diagnostics

| Method | Annualized one-way turnover | Average HHI |

|---|---|---|

| Equal weight | 0.00 | 0.167 |

| Trailing ICIR | 1.64 | 0.172 |

| Hierarchical risk parity | 0.42 | 0.250 |

| Nominal mean-variance | 0.06 | 0.499 |

| CVaR-robust mean-variance | 0.26 | 0.495 |

These results do not show a dramatic robust-optimization advantage. Nominal and CVaR-robust mean-variance produced nearly the same evaluation path, maximum drawdown, and concentration. The robust version recorded a slightly higher annualized return and Sharpe ratio, but also more allocation turnover. With an HHI near 0.5, both solutions spent much of the interval close to the concentration allowed by the 50% sleeve cap. In this case the adverse-scenario penalty adjusted weights at the margin rather than changing the character of the portfolio.

The longer common history supplies a useful counterpoint. From 8 October 2024, nominal mean-variance had the higher annualized return and Sharpe ratio (4.42% and 0.55 versus 4.01% and 0.55 after rounding), while the robust version had the smaller maximum drawdown (6.91% versus 7.67%) and lower annualized turnover (1.59 versus 1.76). The choice of evaluation interval therefore affects which trade-off is most visible, even though the interval was not selected to favor either method.

HRP occupied a different middle ground. It was much less concentrated than the two mean-variance allocations and its weights changed less at adjacent rebalances, but it did not match their risk-adjusted result in the fixed evaluation interval. Trailing ICIR remained close to equal weight in concentration while producing substantially more turnover. A score can vary without producing a useful difference in realized allocation performance.

The practical conclusion is restrained. A tail penalty is informative when it changes an allocation for an intelligible reason—joint losses in adverse observations—not merely because it carries the label “robust.” Here it modestly improved the evaluation Sharpe without reducing the realized drawdown relative to nominal mean-variance. A sensitivity study over window length, risk aversion, tail weight, and grid resolution is required before making a stronger claim.

Reproducibility and limits

The comparison was generated through the same production research engine used to construct and allocate FMPs, but the engine is not part of the argument. The request contract, notebook, derived metrics, figures, and artifact hashes live in the supporting research directory for this Insight. Raw licensed observations and API responses remain outside the website repository.

This is one signal, six related constructions, one historical interval, and one predeclared parameterization. It is not an investment track record and does not establish that one allocator dominates generally. Its purpose is to expose the mechanism: which inputs each method needs, how those inputs alter weights, and whether the observed difference survives costs and a held-back evaluation interval.

Further reading

- Harry Markowitz, “Portfolio Selection”,

The Journal of Finance, 1952. - R. Tyrrell Rockafellar and Stanislav Uryasev,

“Optimization of Conditional Value-at-Risk”,

The Journal of Risk, 2000. - Victor DeMiguel, Lorenzo Garlappi, and Raman Uppal,

“Optimal Versus Naive Diversification: How Inefficient Is the 1/N Portfolio Strategy?”,

The Review of Financial Studies, 2009. - Marcos López de Prado,

“Building Diversified Portfolios that Outperform Out of Sample”,

The Journal of Portfolio Management, 2016. - Jose Blanchet, Lin Chen, and Xun Yu Zhou,

“Distributionally Robust Mean-Variance Portfolio Selection with Wasserstein Distances”,

Management Science, published online 2021. - Yongjae Lee and Daniel Kim,

“Robustness in Portfolio Optimization”,

The Journal of Portfolio Management, 2023.

This walkthrough is for research and educational purposes. It illustrates how strategynet.ai organizes signal evidence into factors and scenarios; it is not a recommendation, investment advice, or an instruction to trade any security.

See plans