US-Israel/Iran conflict (Feb 28 – Mar 9, 2026): from factor shock to a risk-adjusted portfolio

Joint US-Israeli strikes on Iranian leadership and military infrastructure began Saturday, February 28, 2026, with the first trading-day reaction on Monday, March 2. Iran retaliated against US bases in Jordan, UAE, and Qatar. Oil broke $100/bbl for the first time since 2022 on March 9, on roughly 7 million barrels/day of projected regional shut-in risk. Tensions continued well past the initial event window, into July 2026.

This piece traces what factor scores, sector prices, the energy complex, and prediction-market probabilities actually did during that window, drawing on the same production data and factor panel used elsewhere on strategynet.ai, along with a read from Polymarket's public history API. One question follows the retrospective: given a stated view on the energy complex held with some acknowledged uncertainty, what portfolio does that turn into, and what did sizing it carefully actually earn once the event played out?

Background: refining capacity was already tight

U.S. refining capacity remains large by global standards, but it is below its recent peak: operable crude-distillation capacity is roughly 18.1–18.2 million barrels per day, down about 700,000– 800,000 b/d from the 2020 high following several permanent refinery closures. The system has less structural spare capacity than it did before the pandemic, even though the refineries that remain have generally become more efficient and capable of running at high rates.

Refinery utilization rose sharply as the market moved into the summer driving season. Rates that were near 89–91% before and shortly after the conflict increased into the mid-90s by June, with some weekly readings around 96–97%, near the practical upper limit for the national system. Although a 96% utilization rate appears to leave 4% unused, much of that residual reflects maintenance, outages, and units that are technically operable but not immediately available. As a result, the throughput that could realistically be brought online is considerably smaller than the headline spare-capacity figure suggests.

Domestic gasoline demand followed its normal seasonal pattern, rising from winter levels as spring and summer travel increased. Product supplied moved from roughly 8.5 million barrels per day before the conflict to approximately 8.9 million barrels per day afterward. Refiners initially increased gasoline production enough to meet much of this increase, but the rise in output was smaller than the normal seasonal production ramp by early summer. Inventories consequently declined faster than usual, moving from above their five-year seasonal average before the conflict to materially below average by July.

Exports remain an important part of the balance. The U.S. continued to export roughly 0.9–1.0 million barrels per day of gasoline, primarily from the Gulf Coast, even while importing gasoline and blending components into the East Coast. This reflects regional infrastructure and shipping economics rather than a national shortage: the Gulf Coast is structurally long refining capacity, while the East Coast is relatively short and often relies on imports from Europe and Canada. The system overall remained capable of meeting domestic demand, but was doing so with high utilization, reduced inventory cover, and limited room to absorb a major refinery outage or a further increase in demand.

Data

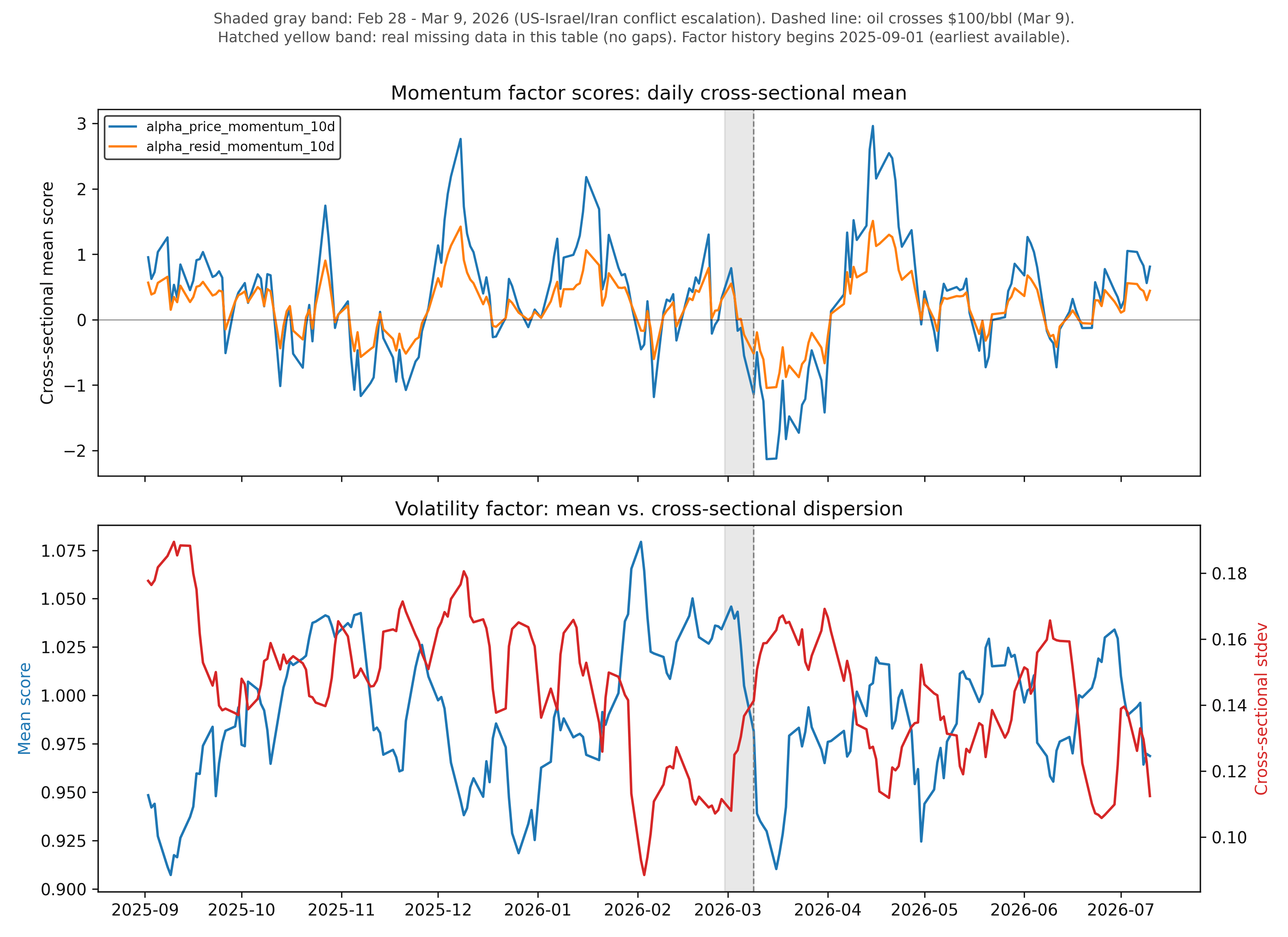

The factor panel is the production nightly feature table, filtered to the momentum/technical/statistical (WQ101) family, the only factor family with a comparable, continuous historical panel on this instance. Prices are daily closes from the same production price table, split-adjusted where a corporate action would otherwise fake a price move (XLE had a genuine 1-for-2 split on 2025-12-05). The context window runs 2025-09-01 to 2026-07-10, about six months before the event and four months after, so the shock reads against a full baseline rather than in isolation.

Momentum crashed harder than any point in the sample

The 10-day price-momentum and residual-momentum factors reversed sign starting March 4-6, 2026, a textbook momentum-crash pattern in which the names that had been trending hardest reverse first and hardest once the regime breaks. Its cross-sectional mean bottomed at −2.13 on 2026-03-13, the single lowest value anywhere in the full 2025-09-02 to 2026-07-10 sample of ten months of daily observations, making it the sharpest momentum reversal in the whole window rather than an artifact of a thin baseline.

The 20-day volatility factor's cross-sectional mean barely moved, but its cross-sectional standard deviation rose about 31% (0.108 to 0.141) from the start to the end of the event window. The shock widened the spread of volatility scores across names more than it raised the average, consistent with a disturbance that hit some names much harder than others rather than lifting volatility uniformly across the cross-section.

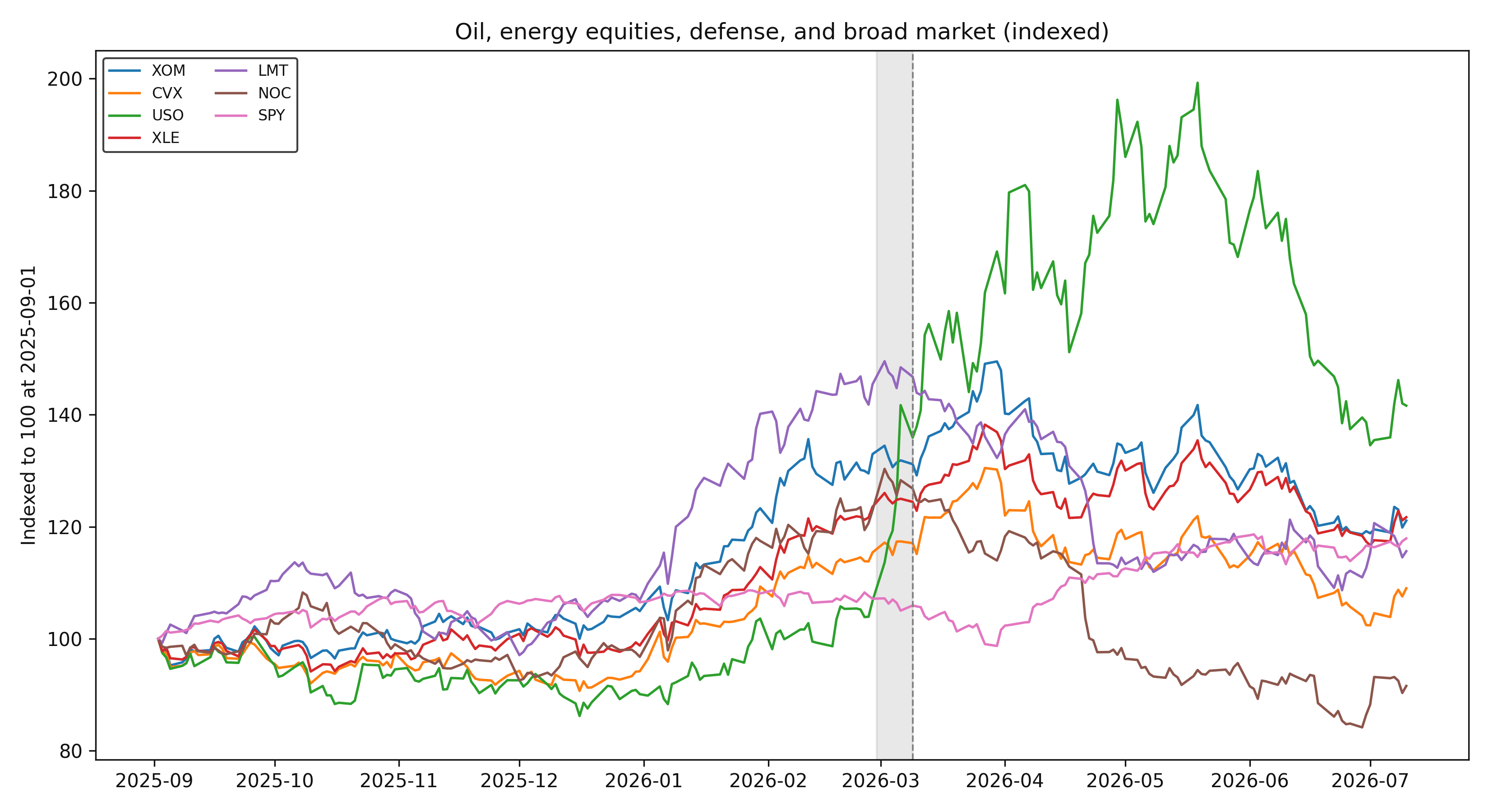

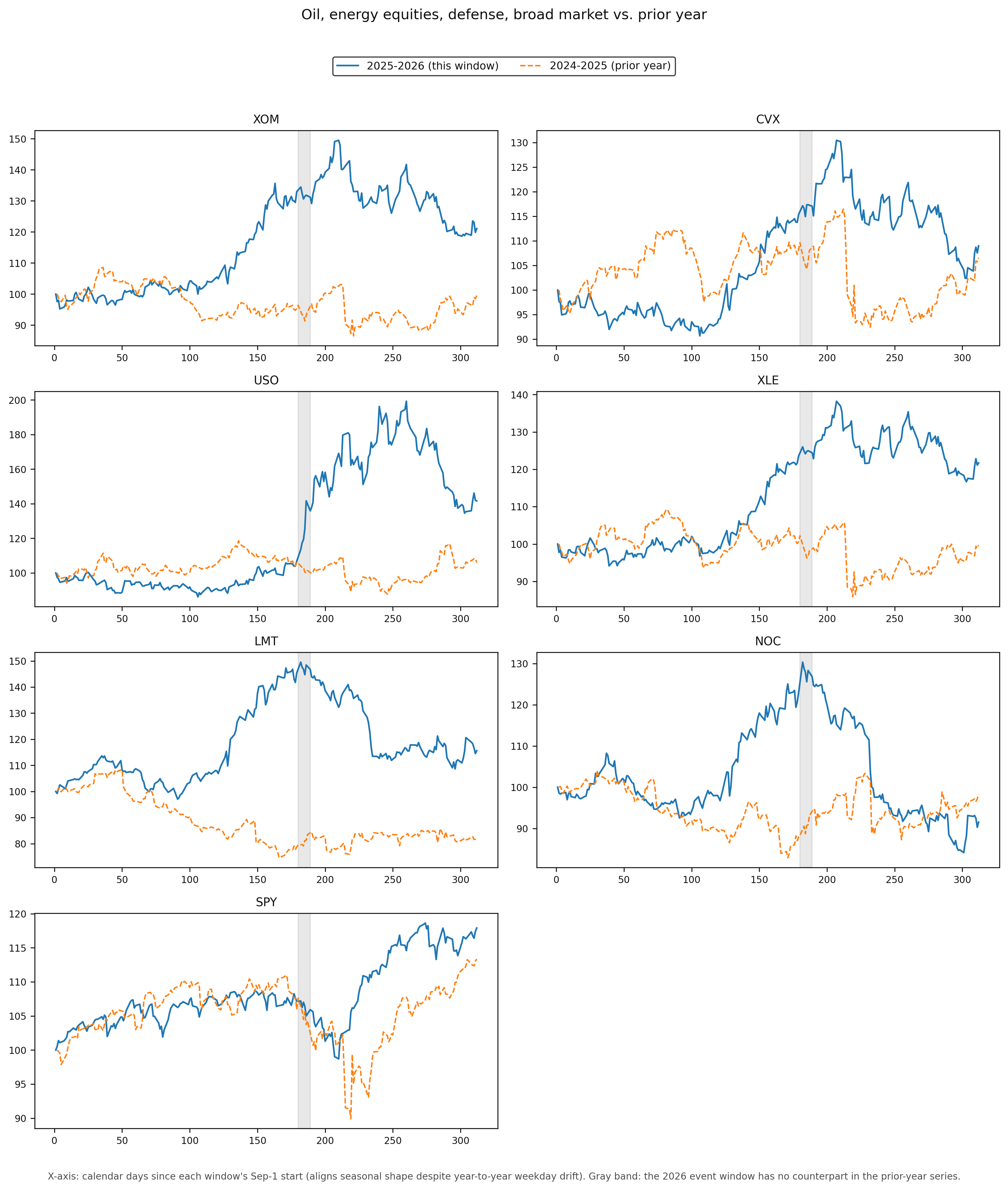

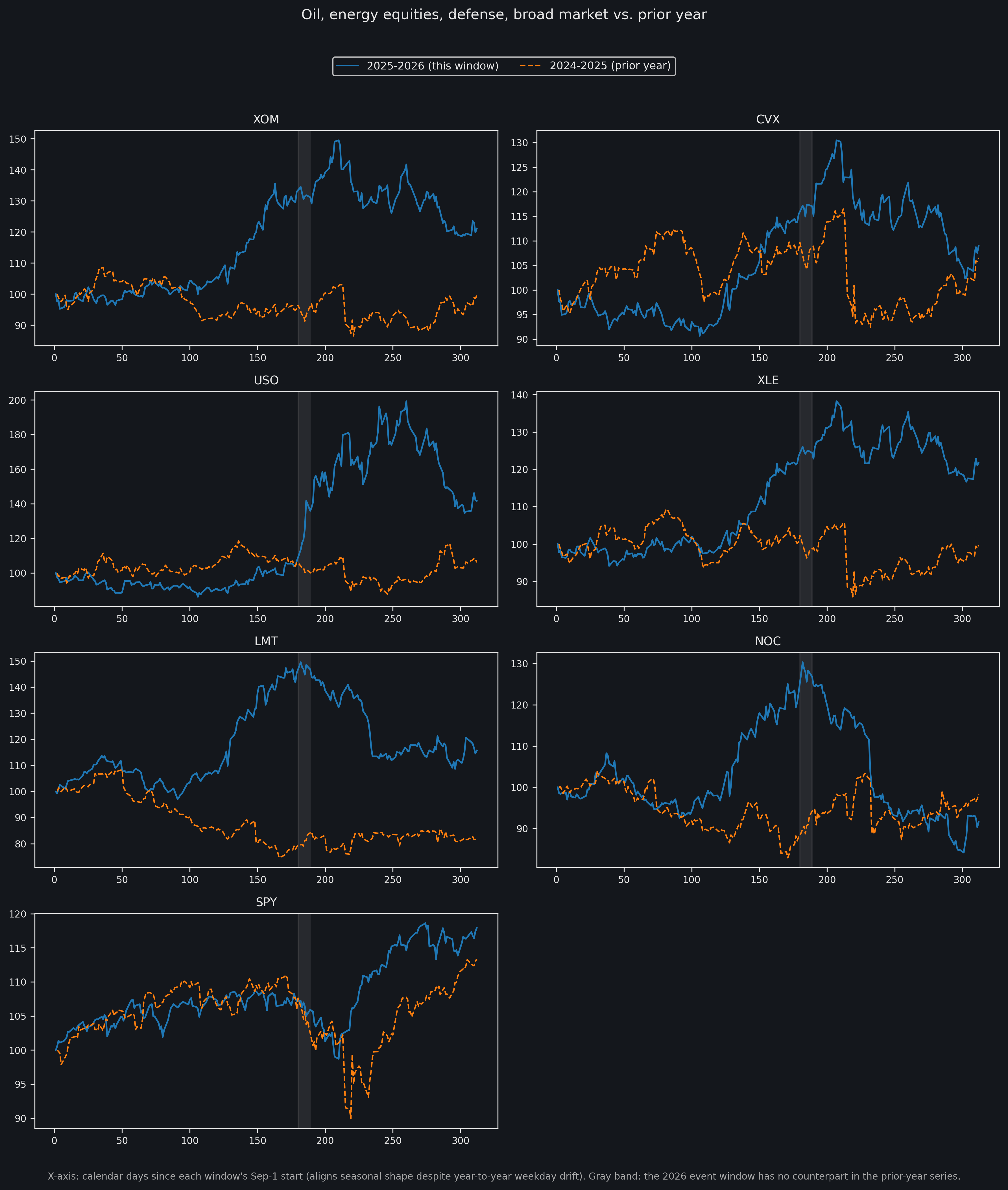

Oil, energy equities, and defense

Oil (USO) diverged sharply from energy equities. USO rose as much as ~99% above its September 2025 baseline by mid-May 2026, while XOM, CVX, and XLE stayed within a much narrower +20% to +35% band for the whole window. The commodity, rather than the equities that produce it, carried almost all of the convexity.

Defense names diverged from each other after the event, which is easy to miss if "defense" is treated as one trade. LMT held its post-event gains into Q2 before fading; NOC gave back its entire post-event rally and ended the window as the worst performer of the whole seven-symbol group in Figure 2, the opposite of the generic "defense up" assumption.

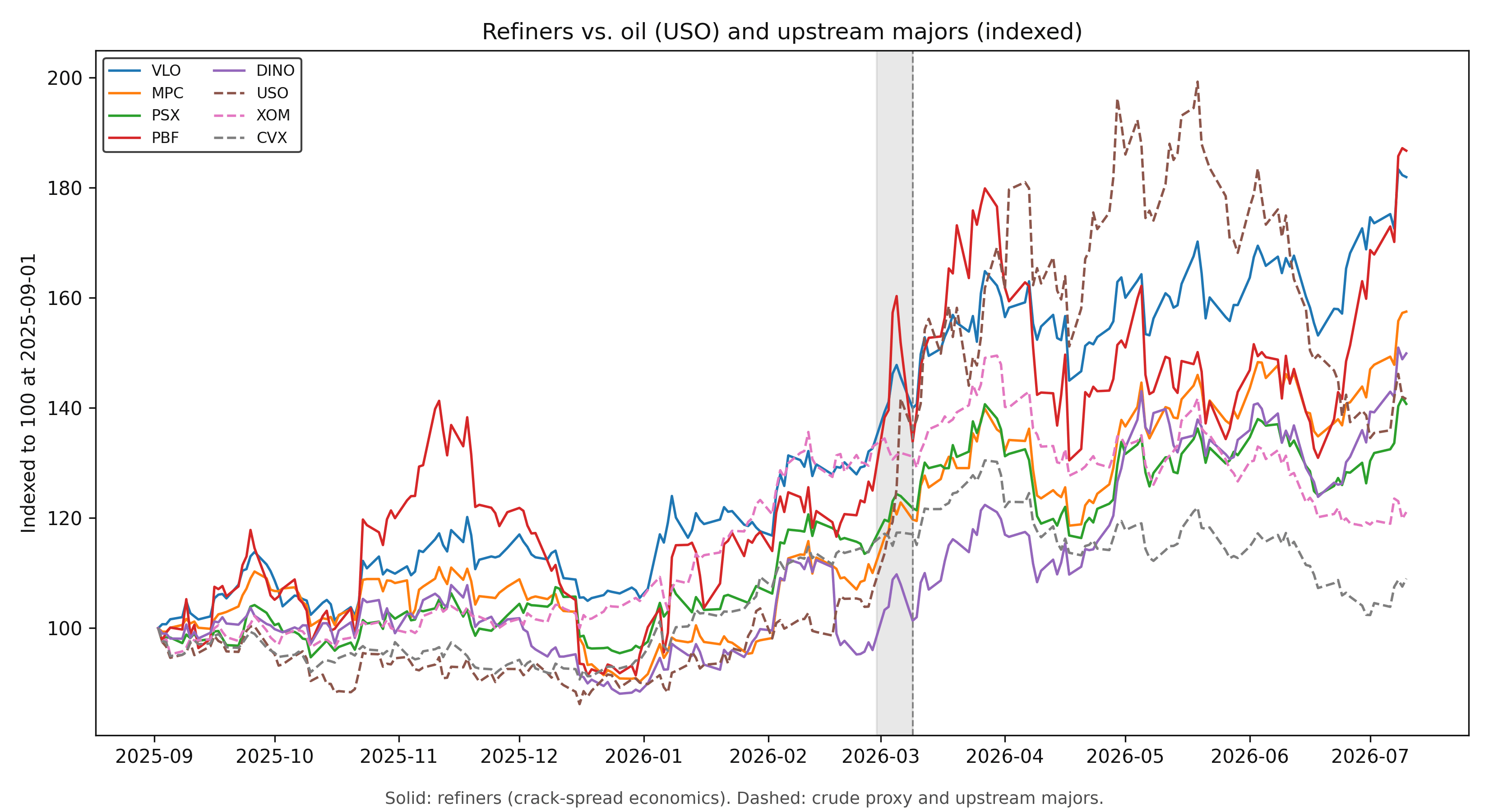

Refiners told a different story than crude or upstream majors

Refiners run on crack spread, the gap between crude input cost and refined product output price, so a supply shock can squeeze their margins even while crude itself rallies. That squeeze story does not hold up cleanly here, and the more interesting result is in the shape of the divergence rather than its direction. USO spiked to its window peak of +99% on 2026-05-19, then gave back most of that move, closing at +42% by 2026-07-10. VLO and PBF climbed more steadily to +82% and +87% and were still near their highs at window end, finishing above USO's ending level despite never matching its peak. XOM and CVX peaked earlier, in late March, and faded hardest of the group, ending at only +21% and +9%. Crude captured the spike; refiners captured the sustained part of the move; upstream majors captured neither by the end of the window.

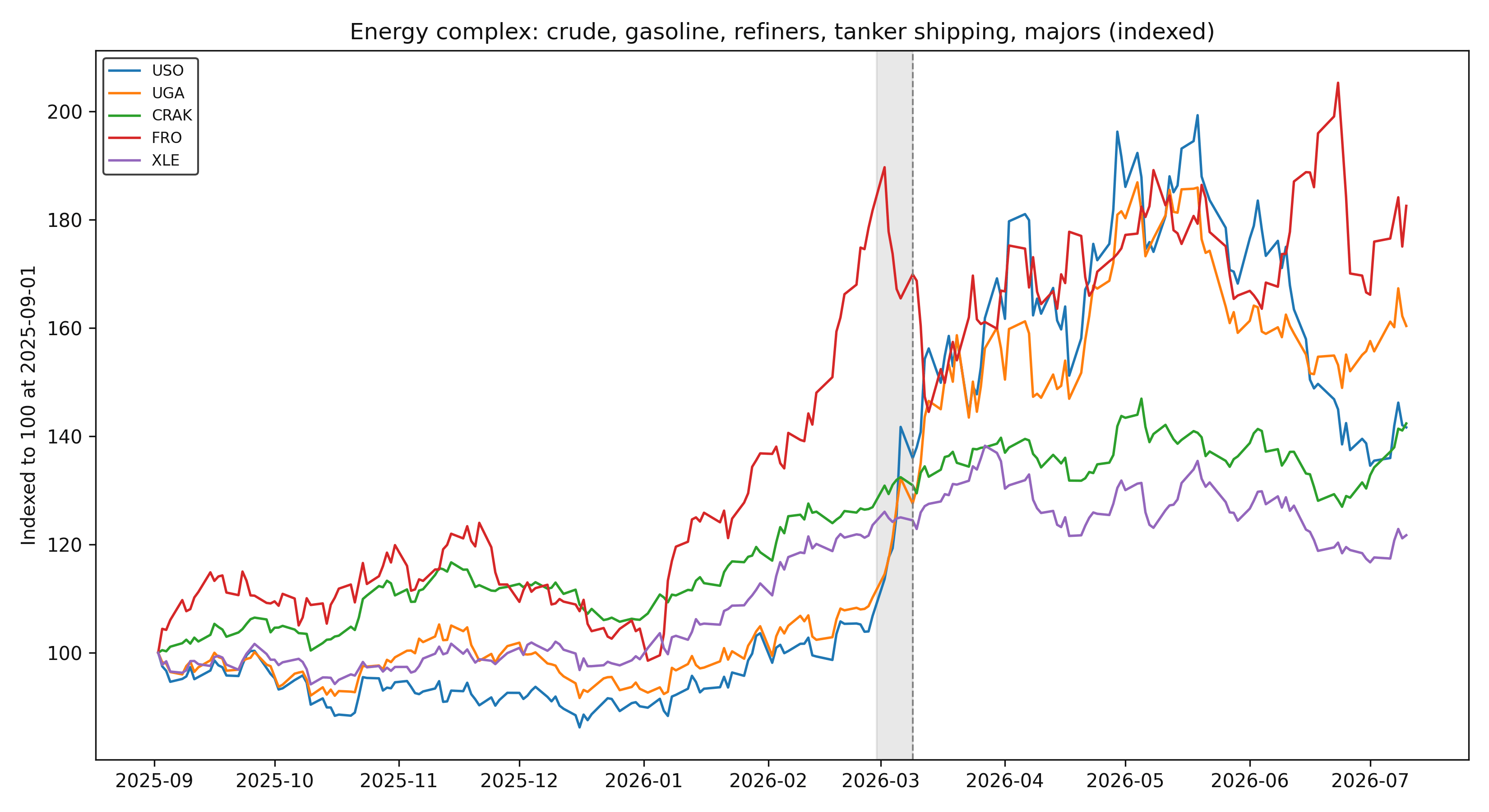

Crude, gasoline, refiners, and shipping diverged

Shipping led rather than lagged. FRO, a large crude-tanker operator, was already +82% above its September-2025 baseline by 2026-02-27, the day before the strikes, a pre-event risk premium that had been building through January and February. It kept climbing to +90% on March 2 (the first trading-day reaction), then gave back most of that move through the rest of the event window, down to +45% by March 13. It then went on to be the best-performing asset of the whole five-asset complex by 2026-07-10, at +82.5%, ahead of gasoline (+60.3%), refiners (+42.3%), crude itself (+41.6%), and diversified majors (+21.7%). Shipping led the move before the event, round-tripped hard during it, then led again for months afterward.

Pre-event correlation of daily log returns (2025-09-01 to 2026-02-27)

| Pair | Correlation |

|---|---|

| USO – UGA (crude – gasoline) | 0.89 |

| USO – XLE (crude – majors) | 0.74 |

| USO – CRAK (crude – refiners) | 0.45 |

| USO – FRO (crude – tanker shipping) | 0.21 |

| USO – BDRY (crude – dry-bulk shipping) | 0.02 |

That last row is the point: "shipping" is not one asset class. Dry-bulk freight (BDRY), which carries iron ore, coal, and grain, is essentially uncorrelated with crude, gasoline, refiner, or energy-major returns; it answers to global industrial demand rather than the Strait of Hormuz. Tanker shipping (FRO) is linked to the same shock, but only loosely, and through a different mechanism: freight rates and war-risk insurance on crude transit rather than the price of crude itself. A single "shipping" line item in a risk model would blend a noisy oil-shock exposure with an unrelated freight cycle.

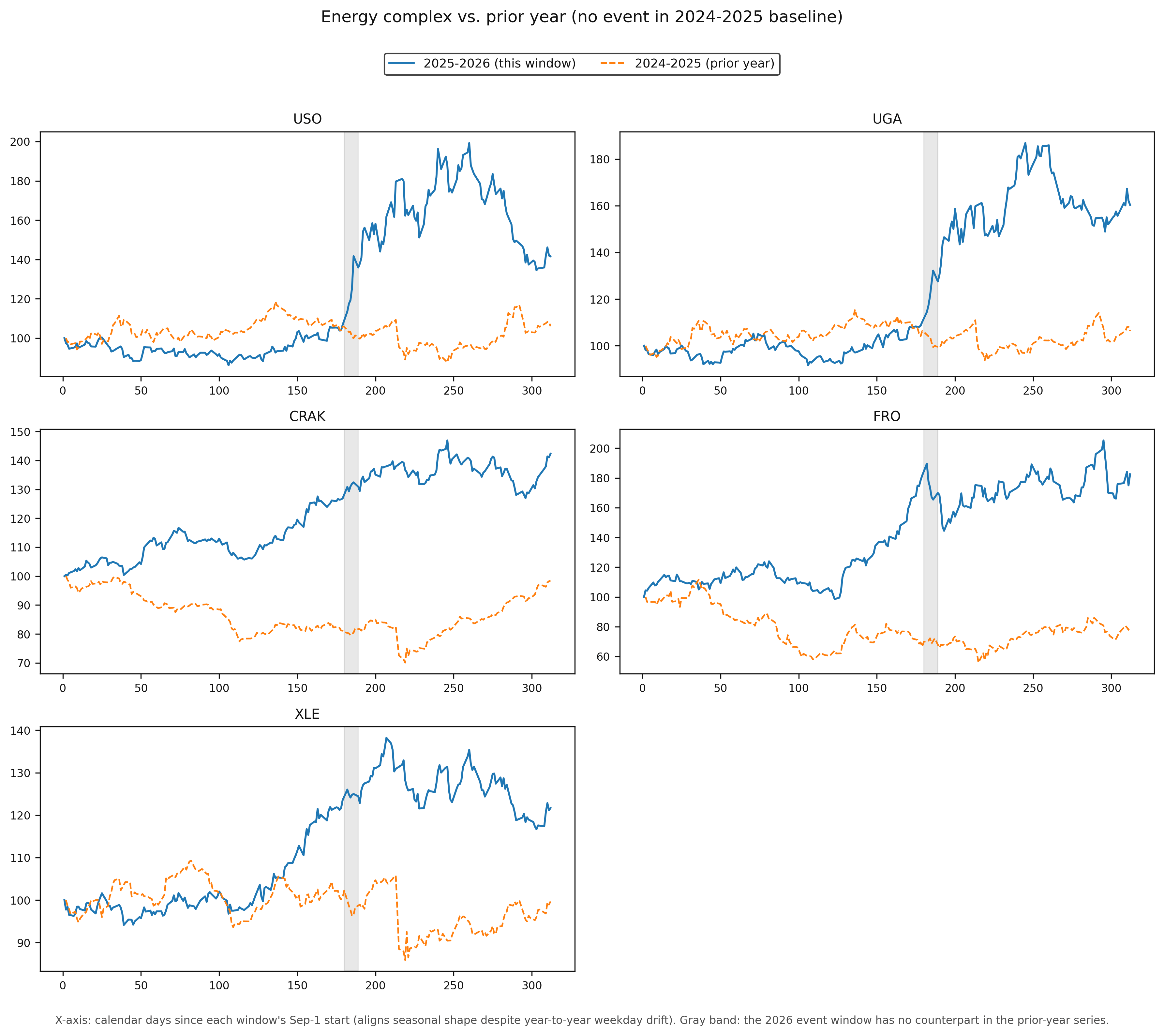

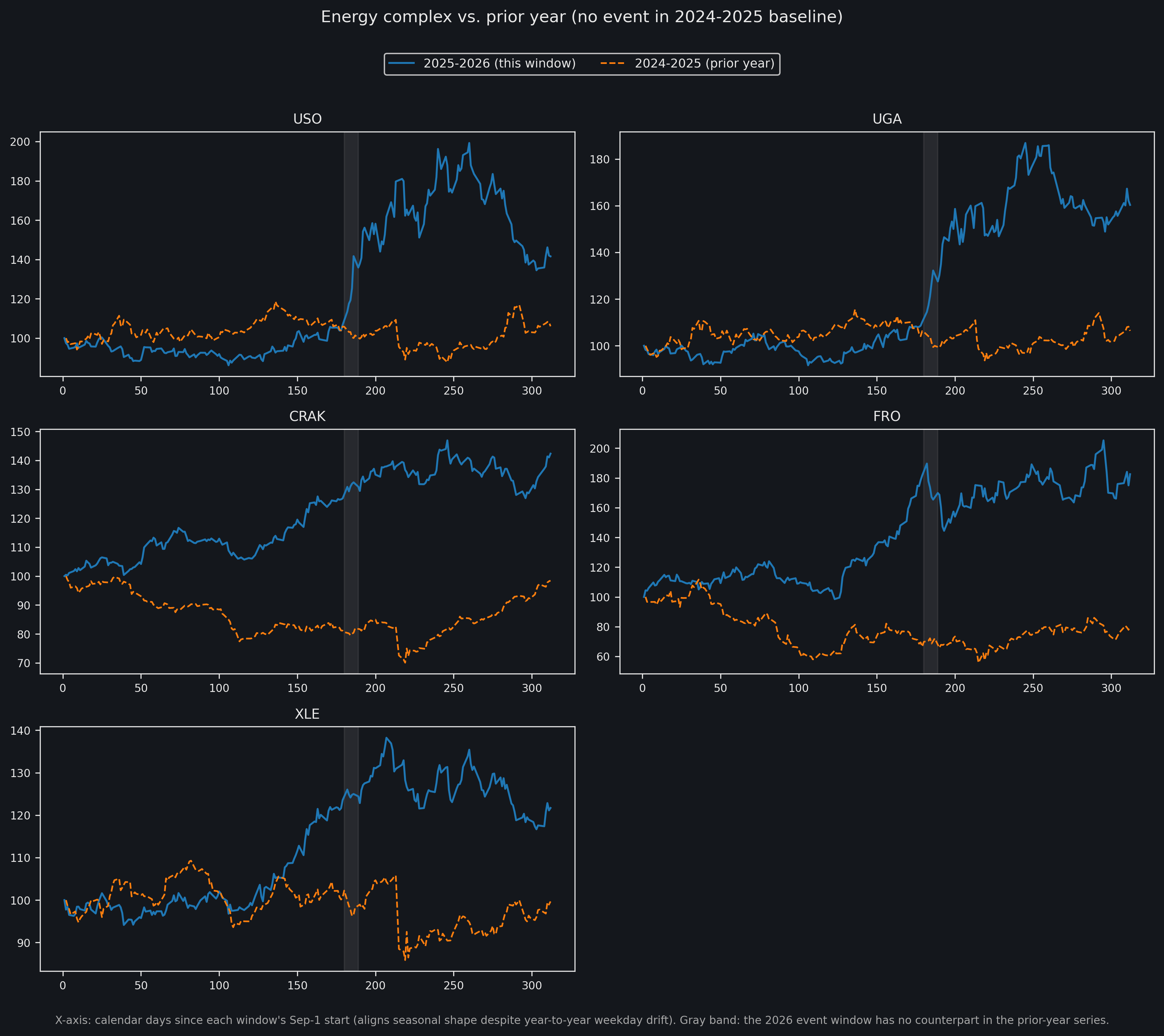

How much of this was seasonal?

The background section above described a seasonal pattern: gasoline demand rises every spring and summer, refinery utilization climbs into the 90s as the driving season approaches, and inventories draw down. That pattern was already in motion when the strikes hit, which raises a fair question: how much of the energy complex's rally is the shock, and how much is just the calendar?

The 2024-2025 window offers a clean answer, since it covers the identical stretch of the calendar with the same seasonal demand pattern and no comparable geopolitical event.

In 2024-2025, all five names stayed range-bound through the same calendar stretch: USO moved between 87.7 and 118.6, UGA between 93.7 and 115.5, XLE between 85.9 and 109.3, and each ended the window close to where it started. In 2025-2026, every one of those ranges was broken decisively. USO reached 199.3, UGA 186.9, XLE 138.2, and none of the five settled back near its starting level. The break happens at the same point on both charts: right at the shaded event window, where the current-year line peels away from a shape that otherwise tracks the prior year reasonably closely through the first several months.

SPY is the interesting exception, and it cuts against a simple "this year was worse" reading. The prior-year window had its own, unrelated drawdown at almost the same point on the calendar, and it went deeper: SPY bottomed at 89.9 in 2024-2025 against 98.7 in 2025-2026, at nearly identical day offsets from each window's start. The broad market absorbed this particular geopolitical shock more calmly than it absorbed whatever moved it the year before.

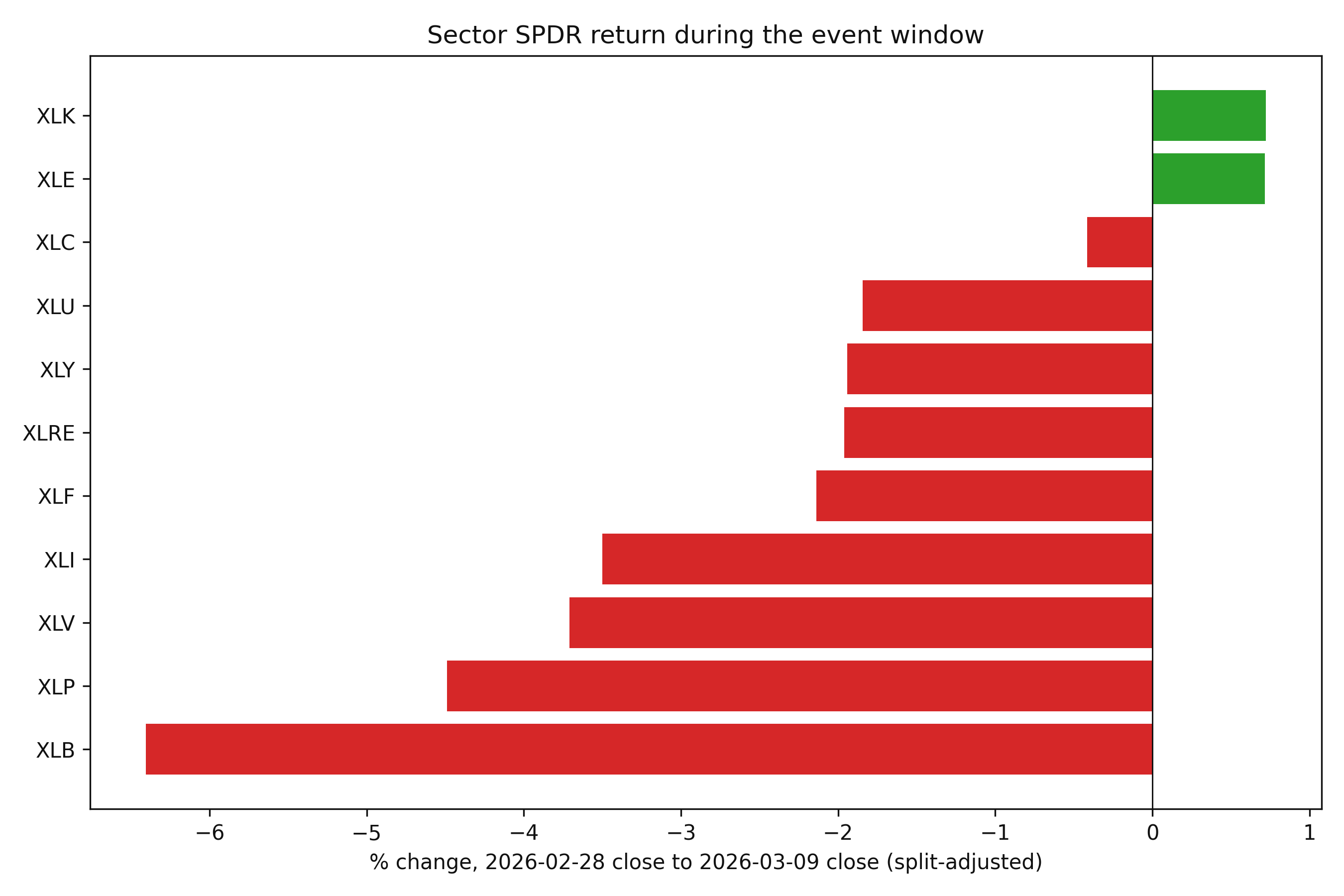

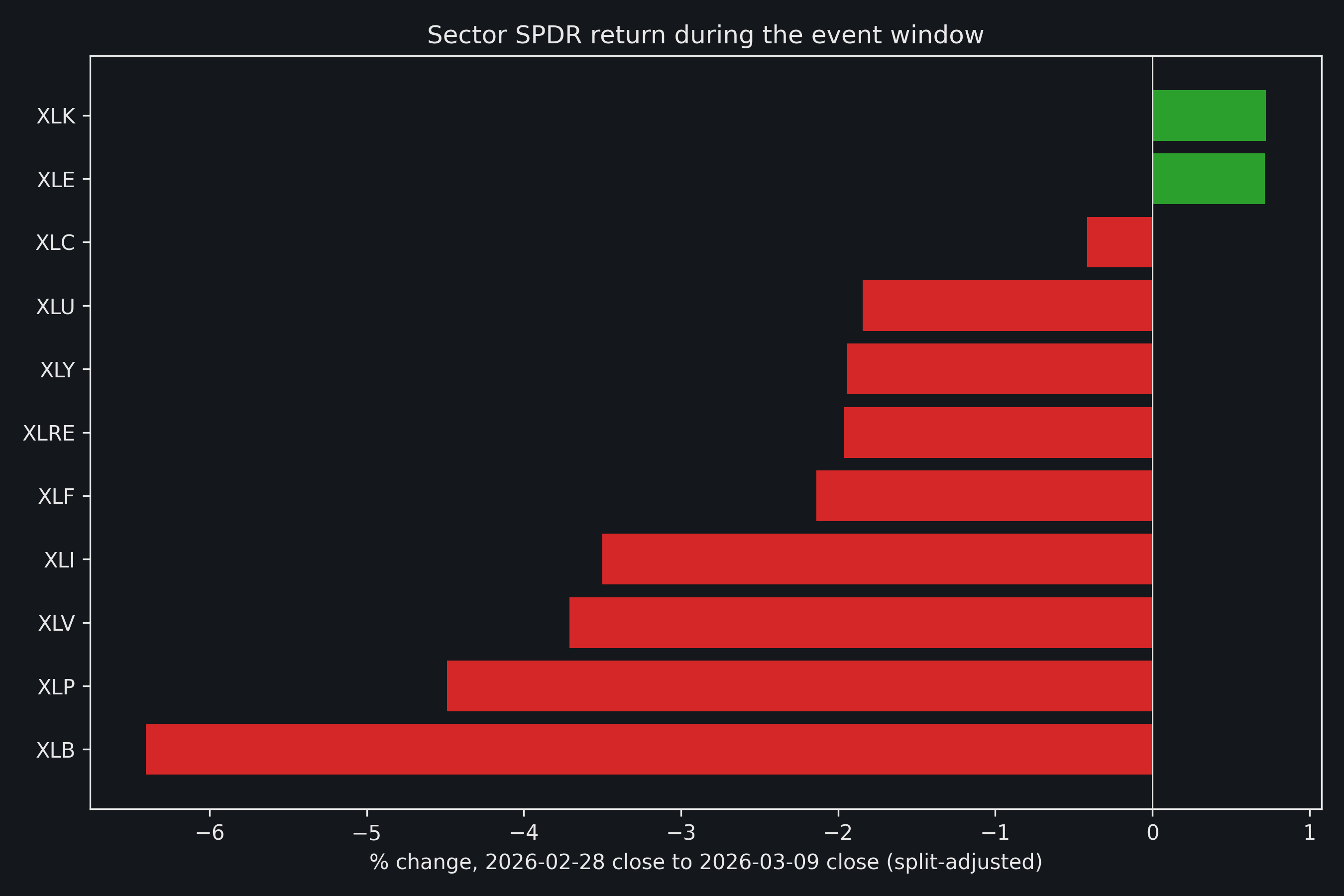

Sector returns during the event window

Sector SPDR returns, 2026-02-28 close to 2026-03-09 close

| Sector ETF | % change |

|---|---|

| XLB (Materials) | -6.40% |

| XLP (Consumer Staples) | -4.49% |

| XLV (Health Care) | -3.71% |

| XLI (Industrials) | -3.50% |

| XLF (Financials) | -2.14% |

| XLRE (Real Estate) | -1.96% |

| XLY (Consumer Discretionary) | -1.94% |

| XLU (Utilities) | -1.84% |

| XLC (Communication Services) | -0.42% |

| XLE (Energy) | +0.72% |

| XLK (Technology) | +0.72% |

Nine of eleven sector SPDRs were negative over the event window itself; only XLE and XLK were positive, and only barely. The bottom of the table is the more interesting part: XLB (materials) was the single worst performer at −6.40%, meaningfully worse than XLP and XLV, and notably worse than XLU (utilities, −1.84%), the sector a defensive-rotation assumption would expect to hold up best in a geopolitical shock. A generic "risk-off, defensives win" story does not survive contact with this table.

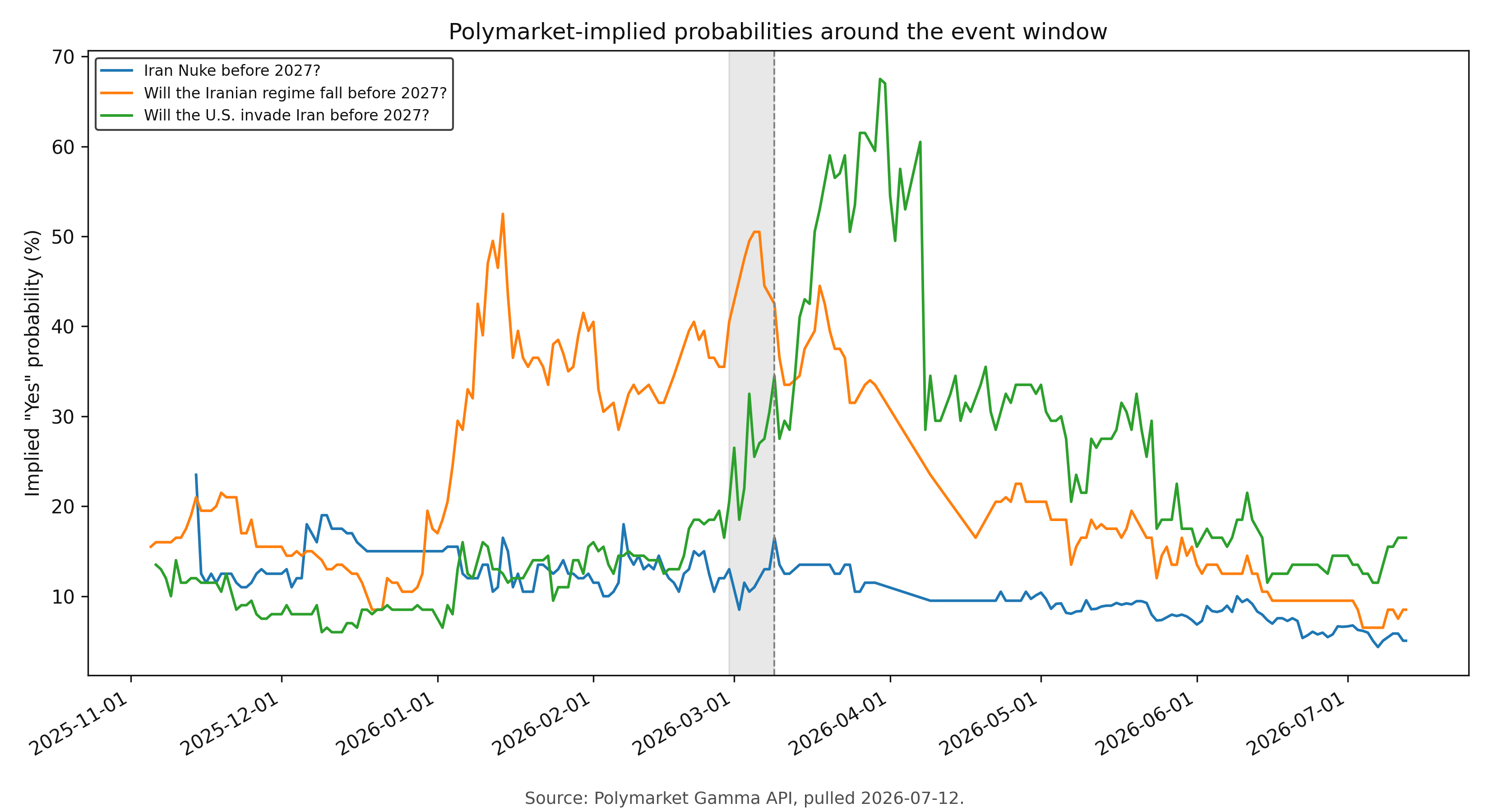

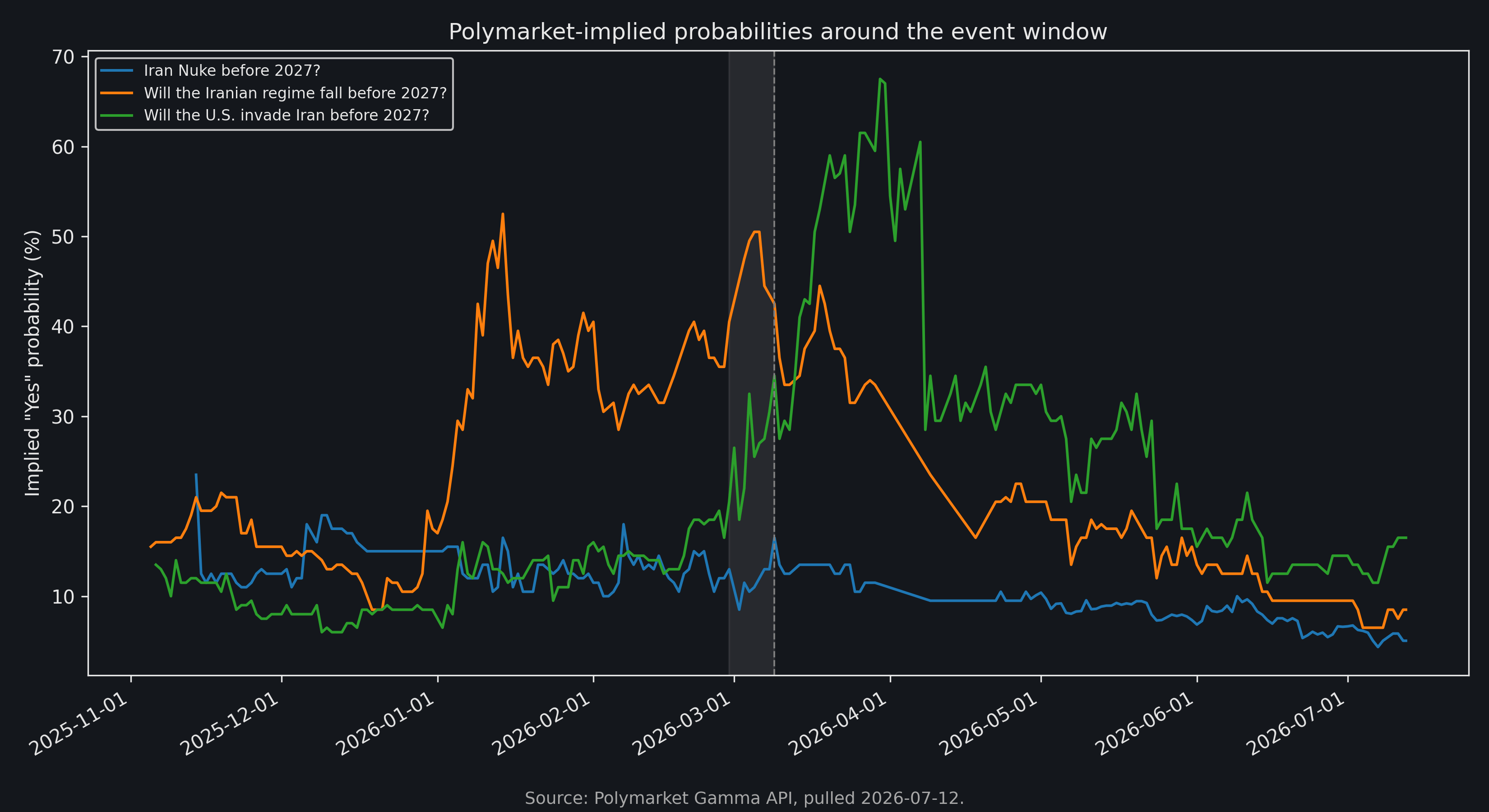

What Polymarket was pricing

This section draws on Polymarket's public history API. Three questions were

selected from a 40-market discovery search as the most directly on-topic

with a clean pre-event baseline: Will the U.S. invade Iran before 2027?,

Will the Iranian regime fall before 2027?, and Iran Nuke before 2027?.

The reaction was uneven across the three, which is itself informative. The invasion question moved from 19.5% (2026-02-27) to 30.5% by the event-window close, then kept climbing for three more weeks to a window peak of 67.5% on 2026-03-30. The crowd's escalation-risk pricing continued rising well past the initial event window, consistent with tensions continuing into the summer. The regime-fall question also moved at the event (35.5% to 43.5%), though its own window peak (52.5% on 2026-01-14) predates the event and isn't attributable to it. The nuclear-test question barely reacted at all (12.0% to 13.0%). By 2026-07-10, both event-reactive markets had decayed well below their pre-event levels, to 16.5% and 8.5% respectively, so the immediate repricing did not persist through the full window the way the momentum-factor and refiner findings above it did.

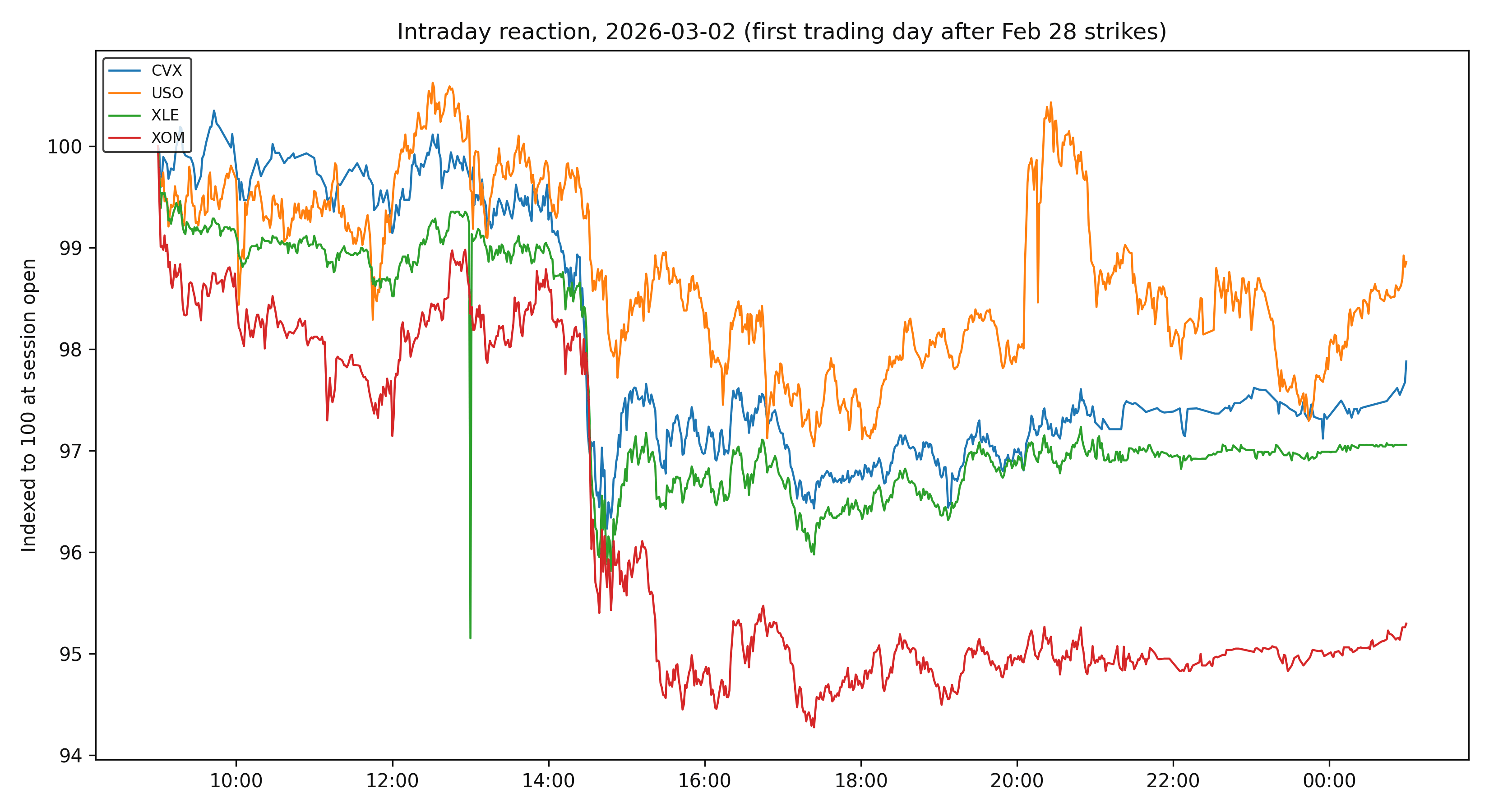

Intraday: a delayed, synchronized repricing

On the first trading day after the strikes, CVX, USO, XLE, and XOM all traded in near-normal intraday ranges until roughly 14:30 ET, then dropped sharply and simultaneously, a delayed, market-wide repricing partway through the session rather than an opening gap. XOM underperformed the other three into the close. Whatever information moved this market on March 2 was not fully priced at the open.

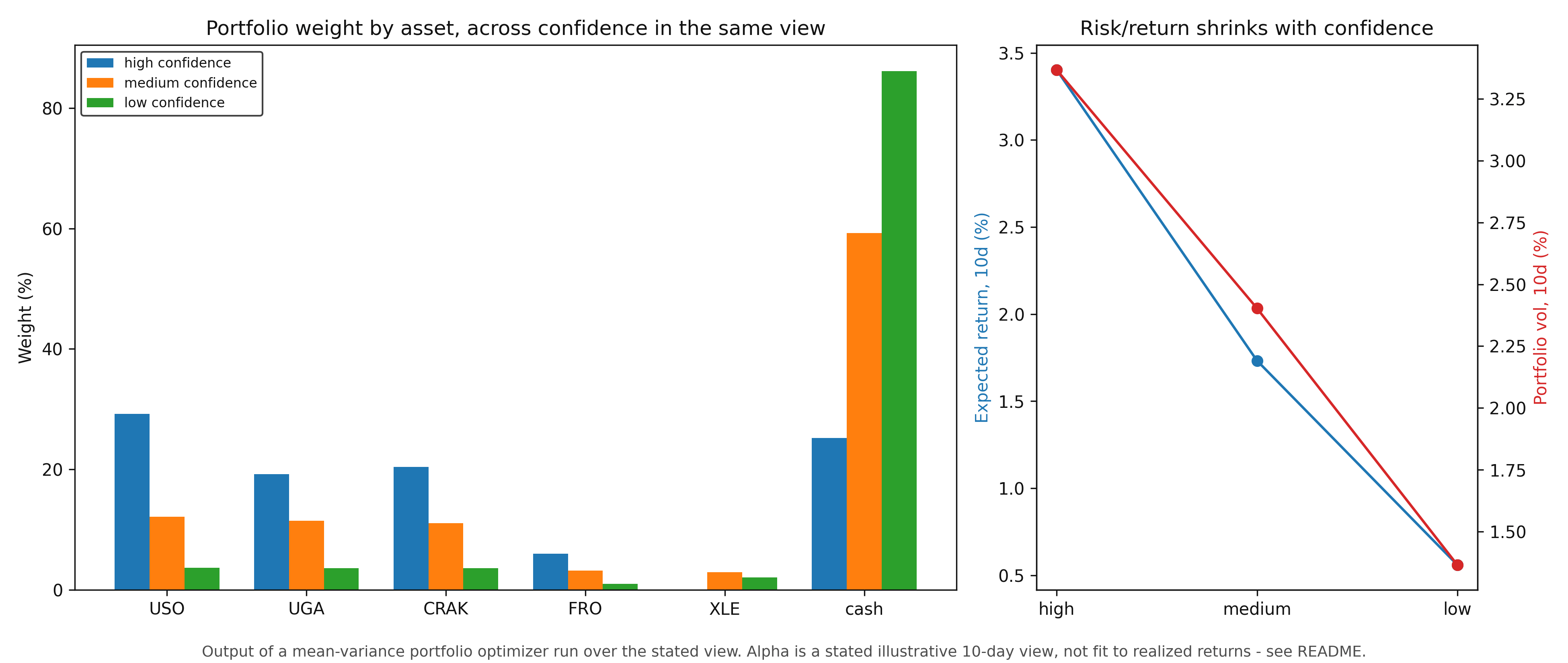

So what: sizing a view under uncertainty

Everything above is retrospective: real evidence about what happened, after the fact. The more useful question is forward-looking. Suppose a desk had a view on the energy complex ahead of an event like this: crude and gasoline most exposed, refiners and majors less so, tanker shipping carrying a transit-risk premium. As with any forecast, that view comes with uncertainty about how right it will turn out to be. What position should it actually turn into, and does sizing it carefully change the outcome?

The mechanism is simple: the less confident the view, the smaller the position, and the difference sits in cash. At high conviction, the portfolio commits about three-quarters of the book to the view; at low conviction, it holds back to under a fifth and sits mostly in cash.

The actual test is what each of those positions would have earned once the event played out, using the split-adjusted price moves already shown above:

What each sized position actually returned

| Position | Cash weight | Event window (Feb 28–Mar 9) | By 2026-07-10 |

|---|---|---|---|

| High confidence | 25.2% | +11.3% | +21.3% |

| Medium confidence | 59.2% | +5.4% | +11.6% |

| Low confidence | 86.2% | +1.8% | +4.9% |

| All cash, no view | 100% | +0.2% | +1.9% |

| Unhedged: 100% crude (USO) | 0% | +27.3% | +32.6% |

Every sized position beat sitting in cash, at every confidence level, over both windows. Even the most conservative position, holding 86% cash, returned +1.8% over the eight trading days of the event window and +4.9% by mid-2026 from a book that was mostly sitting still. The high-confidence position returned +11.3% over the event window and nearly doubled that by mid-year.

The unhedged version of the same trade, putting the entire book into crude alone, returned more than any of the sized positions: +27.3% over the event window, +32.6% by mid-2026. That's the number a simple "oil up" story points to, and on this occasion it beat every risk-adjusted alternative. It was also the version of the trade most exposed to being wrong on the details. Tanker shipping was part of the same thesis, priced with a similarly confident view, and it went negative over the event window itself before its own payoff arrived months later. A desk that had put everything into shipping instead of crude, on the same logic that happened to reward an all-in crude bet, would have opened with a loss and a long wait to find out whether the thesis was even right. Sizing for uncertainty gives up some of the upside on whichever leg happens to work, in exchange for not needing to have picked that leg correctly in advance.

Summary

This episode diverged from the generic version of a geopolitical event story in six ways. Momentum crashed harder here than in any other stretch of a ten-month sample; defense names split rather than moved together; refiners outlasted crude rather than getting squeezed by it; shipping led the move before the event and led it again months later, round-tripping hard in between; materials, rather than utilities, took the worst of the event-window drawdown; and Polymarket's own escalation pricing peaked three weeks after the event before decaying back toward its starting level. Each of those is a checkable claim against a stated table and window, set against a refining system that, per EIA's own reporting, was already running with little spare capacity and thinning inventories before the shock hit.

That evidence turned into a concrete result once it was sized into a position: every confidence level tested here made money, cash included, and the least-confident, most-hedged position of the three still beat cash by a wide margin over both the event window and the following four months. Sizing for uncertainty did not maximize the return on this particular trade; an unhedged, all-in crude bet earned more. What it did was avoid depending on picking the single right leg of the thesis in advance, in a window where the wrong-looking leg (shipping, briefly negative) and the right-looking one (crude) were decided by only a few trading days.

This walkthrough is for research and educational purposes. It illustrates how strategynet.ai organizes signal evidence into factors and scenarios; it is not a recommendation, investment advice, or an instruction to trade any security.

Back to Insights